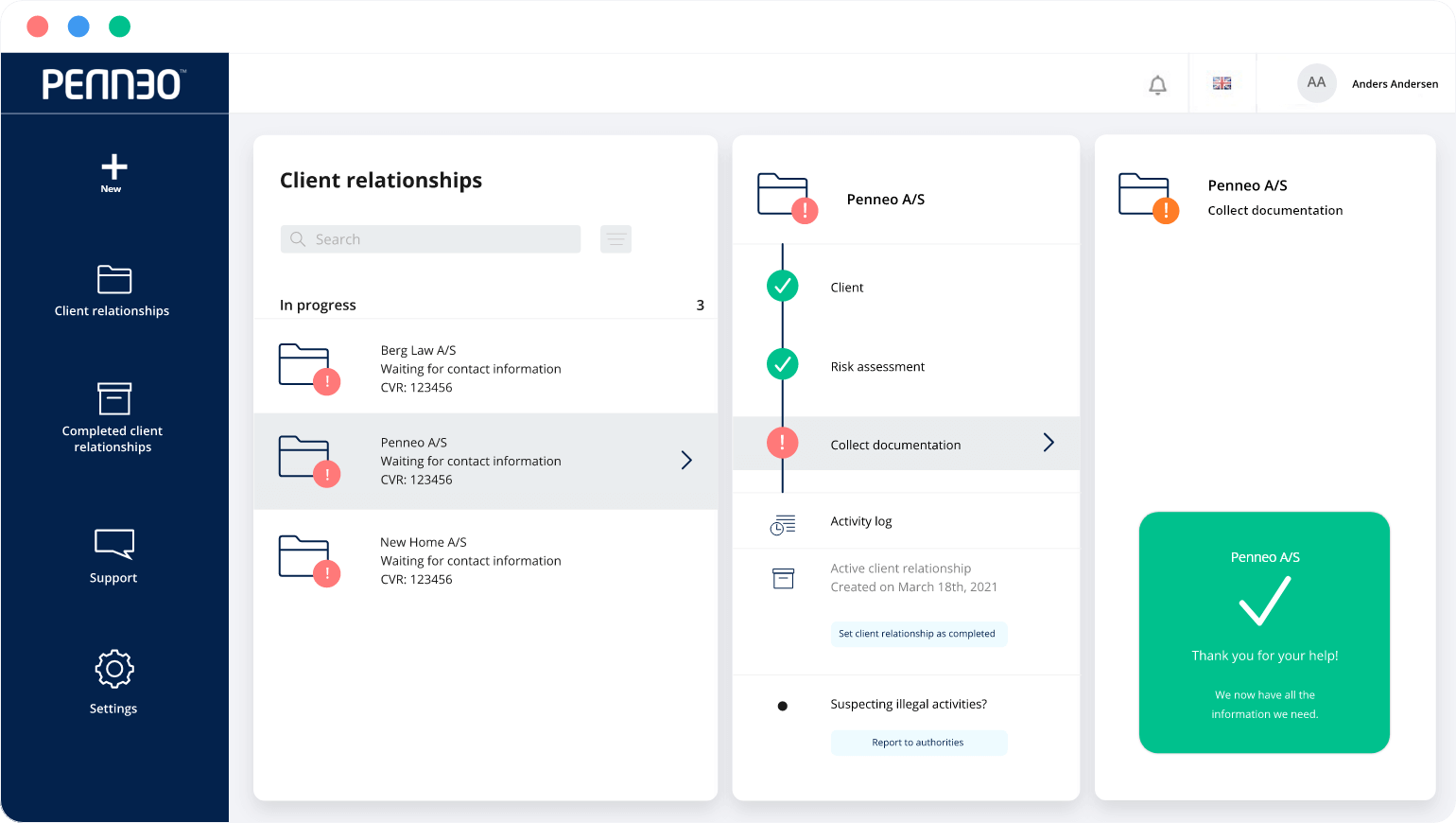

Penneo KYC can help companies that are covered by AML laws to cut down costs, save time, and improve the client experience by automating time-consuming and inefficient KYC processes.

KYC stands for Know Your Customer and is the process of verifying the identity...

Customer due diligence, aka CDD, plays a crucial part in ensuring compliance with Anti-Money...

The EU’s legal framework on anti-money laundering and countering the financing of terrorism (AML/CFT)...